Learn how we are working to transform how we use and produce energy.

Utilities, Analysts, and Customers Agree: Transitioning from Coal Saves Money

There’s a surprising consensus from electric utilities, industrial energy consumers, and financial analysts: transitioning away from coal is good for ratepayers.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Coal economics have eroded dramatically in recent years, so much so that the continued use of existing coal-fired power often imposes a cost burden on electricity customers that exceeds the cost of newer and cleaner sources of power.

Resource planning analyses performed by utilities across the country—including PacifiCorp in the West and NIPSCO in the Midwest—have found that continued operation of existing coal plants is more expensive than the total cost of lower-carbon alternatives. This is true both of gas generation and solar and wind with storage and current federal tax incentives. Climate-focused energy analysts agree, with a recent report from Energy Innovation concluding that 80 percent of coal plants in the United States are more expensive to operate than the cost to build and operate a new wind or solar power facility.

Where coal is being retired and replaced, consumers are seeing rate reductions. One example is in Oregon, where regulators have decided Pacific Power should reduce the rates it charges customers for electricity by an average of about 5.2 percent. About half of that decrease is tied to the lower fuel costs and tax credits that accompany renewable wind and solar power.

And a May 2021 analysis from the U.S. Bureau of Labor Statistics (BLS) shows that since late 2006 electric rates in regions with high coal reliance have increased at a notably faster pace than rates in areas with cleaner resources. This is despite the retirement of nearly 100 gigawatts (GW) of coal capacity between 2008 and today. The BLS points to surging coal fuel prices, which rose 93 percent between 2004 and 2019, compared to a more modest 49 percent increase in retail electricity prices. As coal plants age and their fuel costs increase, the remaining coal fleet will face increasing economic headwinds, resulting in higher prices for consumers.

Electric utilities, large industrial energy users, climate advocates, and financial analysts don’t typically agree on much. But there’s a surprising consensus building among these diverse stakeholders: transitioning away from coal is good for ratepayers.

Why are We Still Burning Coal?

While the poor economics of coal are increasingly clear, over 225 GW of coal generation continues to operate in the United States, of which almost 200 GW does not have a retirement date before 2030. And while most remaining plants operate less frequently than they did in the past, reduced output only partially reduces coal’s cost burden on consumers.

For utilities with cost-of-service regulation, investment costs and related financing charges (together, “capital costs”) are paid for by customers in their electricity rates even if plant utilization declines. Indeed, as output falls, the capital costs embedded in each unit of electricity will rise. To escape coal’s rising operational costs and mitigate legacy fixed costs, plants must be retired and their unrecovered investment costs refinanced using proven tools such as securitization that eliminate expensive equity and command the lowest interest rates.

Why are the Economics of Coal Eroding?

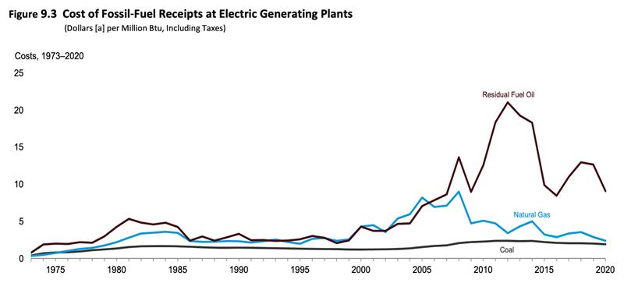

First and foremost, the costs of other power sources have fallen steeply over the last decade and a half. Natural gas fuel costs have declined from $35–$55 per megawatt-hour (MWh) in 2010 to $20–$30/MWh today, directly competitive with the fuel cost for coal of $20–$25/MWh. And gas plants also have lower capital costs than coal plants.

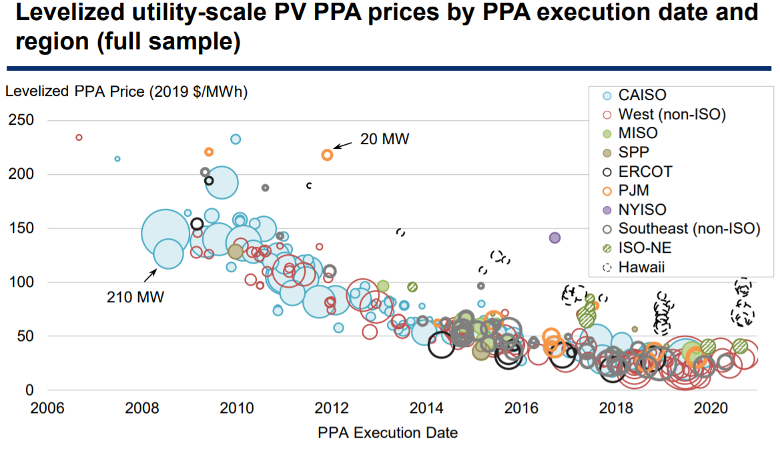

Over the same period, the cost to build and maintain solar, net of currently available federal tax credits, has fallen by around 90 percent, from $200/MWh to $20–$25/MWh. This means the cost to build and maintain solar is comparable to coal fuel prices alone. New wind is even cheaper, with Xcel Energy’s landmark request for proposal in 2017/2018 garnering median bids of $18/MWh. At these prices, wind and solar can undercut existing coal plant operating costs even when additional transmission and integration costs are accounted for.

Source: Berkeley Lab, Utility Scale Solar 2018 Edition

Second, as gas and renewable generation costs have fallen, the cost to operate a coal plant has increased, driven by rising fuel costs and by operational inflexibility. Coal plants can be difficult to ramp up and down, and doing so often reduces their efficiency and places additional wear and tear on the equipment. Such inflexibility can lead to plants being left to run even when their operating costs exceed the market revenue they receive for their generation.

Source: EIA Monthly Energy Review, June 2021

A recent analysis completed by the MISO Independent Market Monitor found that, between 2017 and 2019, 12 percent of coal generation was dispatched uneconomically— thereby losing customers money. This result is in line with similar studies by the Sierra Club and the Union of Concerned Scientists, which show that uneconomic coal dispatched out of merit order has cost utility ratepayers across the country billions of dollars in recent years.

Third, new investments in remaining coal plants over the last fifteen years, in part to mitigate harmful pollutants from coal combustion, have significantly increased ratepayer costs. The value of coal and steam gas assets on utility books has more than doubled from $42 billion in 2005 to nearly $96 billion today, even as installed capacity fell from 150 GW to 126 GW. As noted above, due to cost-of-service regulation, these costs are borne by ratepayers.

Increasing investment into a diminishing coal fleet means the ratepayer burden for steam plants has nearly tripled since 2005, from $234 million per GW to $626 million per GW. Over the same period, coal plant utilization has dropped from 68 percent to 45 percent, which means that utility customers are stuck paying higher capital costs on plants providing less energy.

Fourth, these challenges persist even in regions with capacity markets that compensate coal for its contribution to system reliability. Coal plants fared worse than any other fuel in PJM’s most recent capacity auction. Coal-fired capacity clearing the market dropped by over 8 GW compared to the previous auction, while the amounts of gas, nuclear, renewables, and energy efficiency all increased.

Coal plants even struggled to clear despite the new Minimum Offer Price Rule (MOPR) which penalizes renewable and nuclear generators for benefitting from state subsidies. An analysis by BloombergNEF following the auction found that 38 GW of PJM’s 48 GW of coal would be unprofitable in 2023. Credit rating agency Moody’s issued a similar warning that the low auction clearing price “likely accelerates coal plant retirements.”

These forecasts are already bearing out, with NRG announcing on June 17 that, based on the results of the auction, it will retire two coal plants in Illinois and one in Delaware that together account for 55 percent of the company’s coal-fired capacity in PJM.

Utilities Take Notice

As coal power exerts upward pressure on retail power rates, utility executives are speaking out about how a smart transition away from coal is benefitting their customers:

- “Despite all of these advantages that we have with Coal Creek Station, we lost $170 million in 2019 on energy sales. And looking forward we don’t see market conditions improving to a point where we can keep the plant operational.” – David Saggau, CEO, Great River Energy

- “In many cases, building a new renewable is cheaper than the variable cost of the fuel.” – Andrés Gluski, President and CEO, AES

- “[Retiring and replacing coal plants with renewables will save] somewhere in the neighborhood of $4 billion for our customers…. It gets us out of coal in ten years, and it’s really driven by economics.” – Mike Hooper, Senior Vice President, Northern Indiana Service Company (NIPSCO)

- “As market conditions continue to change the mission of fossil plants, Evergy coal plants will run for fewer hours as their energy is increasingly displaced by lower cost renewable resources.” – Evergy press release

- American Electric Power representatives acknowledged that shutting the Mitchell coal plant down 12 years ahead of schedule could save ratepayers more than $300 million.

- In June 2021 “Consumers Energy…announced a sweeping proposal to stop using coal as a fuel source for electricity by 2025—15 years faster than currently planned. The plan would make the company one of the first in the nation to go coal-free and provide a 20-year blueprint to meet Michigan’s energy needs while protecting the environment for future generations…[and] save customers about $650 million through 2040.” The plan still requires regulatory approval.

Industrial Consumers Join In

Heavy manufacturers and other industrial users of electricity stand to benefit from lower-cost energy. Increasingly these companies see this coming from non-coal sources. Diversifying the electricity supply in coal-heavy states can lead to lower and more stable rates that are decoupled from aging plants and volatile fuel markets, all of which means lower production costs and greater manufacturing investments:

- “Our estimate of the subsidies for the two OVEC coal plants for the entire term of the subsidy created by House Bill 6 is approximately $700 million. This cost comes with no benefit to customers.” – Ohio Manufacturers Association testimony to the Ohio General Assembly

- “Although it is a given that the regulated monopoly utilities and the interests that support traditional coal-fired power plants and other fuel sources will remain well represented in any consideration of West Virginia’s energy future […] it simply defies common sense that West Virginia’s electric rates are not more competitive regionally and nationally.” – West Virginia Energy Users Group 2021 newsletter

The Path Forward

At its peak, coal supplied the majority of electricity for the United States. But as competing sources of power fell in cost and proliferated on the grid, it became a less important resource. Today, cleaner fuels and technologies can ensure reliability at lower cost. An RMI analysis found that by 2025, 27 percent of the coal fleet will be able to retire without need for replacement and an additional 29 percent can retire with wind and solar replacing energy services.

Carbon capture and storage (CCS) is often cited as a possible solution for preserving coal plants within a decarbonized power system, and CCS might provide dispatchable generation in an electricity sector with more variable resources. However, the economic and environmental cases for this approach are not compelling at this time.

CCS technology has been successfully demonstrated at one US coal power plant, thanks to sizable financial support from the both US and Japanese governments. However, this project’s business case was premised on the use of captured carbon dioxide (CO2) for increased oil production. In effect, this project seeks to lower the cost of production of one fossil fuel (petroleum) to cover the added costs needed to capture carbon from another (coal).

Without additional revenue from oil production, some combination of tax credit support for CCS and any additional capacity or grid reliability benefits of coal must exceed the incremental cost of CCS just to bring coal plants back to today’s often uneconomic starting point. The recently expanded federal 45Q tax credit is set to provide $50 per metric ton of geologically sequestered CO2 at mid-decade and could, in principle, help with the economics.

However, other firming technologies pioneered by US companies, such as storage and electric vehicles (EV), can provide the same services at ever lower costs and with less risk. US firms are already global leaders in battery storage and EV technologies. This is not the case for CCS, for which foreign companies like Japan’s Mitsubishi Heavy Industries lead the field. It is also not the case for PV panel manufacturing, which is now dominated by Asian firms—with the exception of First Solar, which is now expanding its facility in Ohio.

Nevertheless, panels have become so cheap that the bulk of the economic benefit of a solar farm is in the balance of system costs, which are spent on U.S. goods and services. In addition, battery storage and EV do not present investors with risks associated with the efficacy and safety of long-term geological carbon storage—and the associated uncertainty in 45Q tax benefits tied to carbon storage performance.

For a century, coal power was a critical grid resource and played an important in the development of our economy. But today, coal power is a driver of higher energy costs and a damper on economic growth. To unleash the next wave of investment and job growth, America should take a proactive yet equitable approach to the energy transition in coal-heavy regions. Rather than propping up uneconomic coal plants and further increasing rates, the United States should embrace the energy transition with support for coal-dependent communities to thrive in a low-carbon economy.

Learn more about the challenges and opportunities of energy transition in the utility sector by exploring RMI’s Utility Transition Hub (https://utilitytransitionhub.rmi.org/). To stay up to date on the latest RMI insights and data releases on the utility transition, subscribe to the Hub’s mailing list (https://utilitytransitionhub.rmi.org/#subscribe).

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.