Learn how we are working to transform how we use and produce energy.

The Right Nudge: Targeted Interventions to Accelerate the Technology Shift in Buildings

How financial institutions can help building decarbonization technologies reach key tipping points.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Our previous blog post presented the financial sector’s opportunity and obligation to lead the way in decarbonizing the built environment in the United States. But what does that mean? After all, the financial sector is multifaceted, and there are many potential intervention points in real estate.

It is not technological breakthroughs we need. For the most part, buildings already have all the tools they need to decarbonize. What we need is a common framework for building decarbonization and an understanding of the ways in which new technology has historically displaced the old. Then, we can illuminate the way forward for finance to accelerate that displacement in order to rapidly and efficiently eliminate the 13 percent of US emissions that come from building operations today.

Converging on One Framework for Building Decarbonization

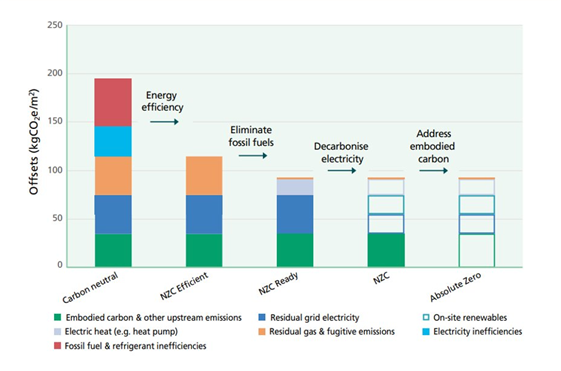

Exhibit 1: Variances in Building-Level “Zero Carbon” Definitions

In real estate, there is no one broadly accepted framework for a net-zero building. One way to think about building decarbonization is in terms of phased removal from building operations and construction: first, removal of emissions associated with inefficiencies in both electric and fossil fuels; then complete electrification, which removes emissions from any remaining fossil fuels; then removal of emissions associated with nonrenewable electricity; and, finally, removal of emissions due to embodied carbon (Exhibit 1 above). In other words, this is how we get from the status quo to absolute zero in the next 28 years in order to reach net zero by 2050 and align with a 1.5oC trajectory. For financial institutions to target effective net-zero financial solutions toward this goal, it is critical to first have a systematic framework that defines what a green building is and delineates various stages on the journey to achieve that designation.

Carbon Neutral

The column to the far left represents real estate as it exists today. Carbon neutrality is achievable in multiple ways. For instance, a portfolio owner could make their real estate portfolio carbon neutral by buying carbon offsets. But even if the carbon offset market were reliable and efficient — which it is not — this would require purchasing offsets equivalent to 13 percent of US carbon emissions. That is clearly not an option.

Net-Zero Carbon (NZC) Efficient

A far more effective method would be to eliminate emissions due to inefficiencies in building operations, leading to the next step in the chart – NZC efficient. The real estate industry has been doing this work for over 20 years, and the technology needed to accomplish it is both well-established and generally price competitive. Almost every professional real estate company focuses on efficiency to some extent because it contributes directly to the bottom line.

Net-Zero Carbon (NZC) Ready

To get to NZC readiness, fossil fuels must be eliminated by electrifying the entire building. A common step would be to replace gas furnaces with heat pumps. Until relatively recently, they were not as reliable or cost-effective as natural gas furnaces. However, advances in heat pump technology have made them a superior product from a health and reliability perspective. Increased demand for heat pumps — fueled by the recently passed Inflation Reduction Act — will help push the industry along the learning curve (explained below), driving down prices so that heat pumps will supplant gas furnaces as the industry standard in the not-so-distant future.

Net-Zero Carbon (NZC)

In this stage, buildings have eliminated all emissions due to inefficiencies, have fully electrified, and only use electricity from renewable sources. The only remaining source of emissions is embodied carbon associated with building materials and construction processes.

Absolute Zero

Finally, to get to absolute zero, we would need to remove embodied carbon from the construction of buildings.

Accelerating the Needed Technological Shift

The technology to move buildings through these phases toward absolute zero is already readily available, but zero-carbon technologies have yet to become the mainstream choice. If we have the technology, why are buildings still inefficient and reliant on fossil fuels? Technological shifts take time, even when they are inevitable. To hasten this shift for buildings, given the rapidly dwindling time to get on track for a 1.5°C trajectory, we need to use the right levers to make the already existing decarbonization technologies cheaper and therefore the default choice, instead of trying to convince purchasers to choose the efficient option even if it is more expensive.

The good news? History shows us that once change starts, it happens fast. All we need to do is nudge it in the right direction.

Making Green Options Cheaper Increases Adoption

RMI’s theory of change in the real estate sector is based on the learning curves in Exhibit 2 above, as well as the power of the market to hasten adoption of new technologies while eliminating older technologies. So how do we make the green option the cheaper, default choice? By enabling pertinent financial actors to provide targeted interventions.

Targeted Interventions Drive Change

Real estate is larger and more diverse than other hard-to-abate sectors. To understand which levers can help speed up the adoption of existing green technologies and arrive at actionable interventions that focus on actual carbon emission reductions, we undertook a detailed segmentation analysis of the sector.

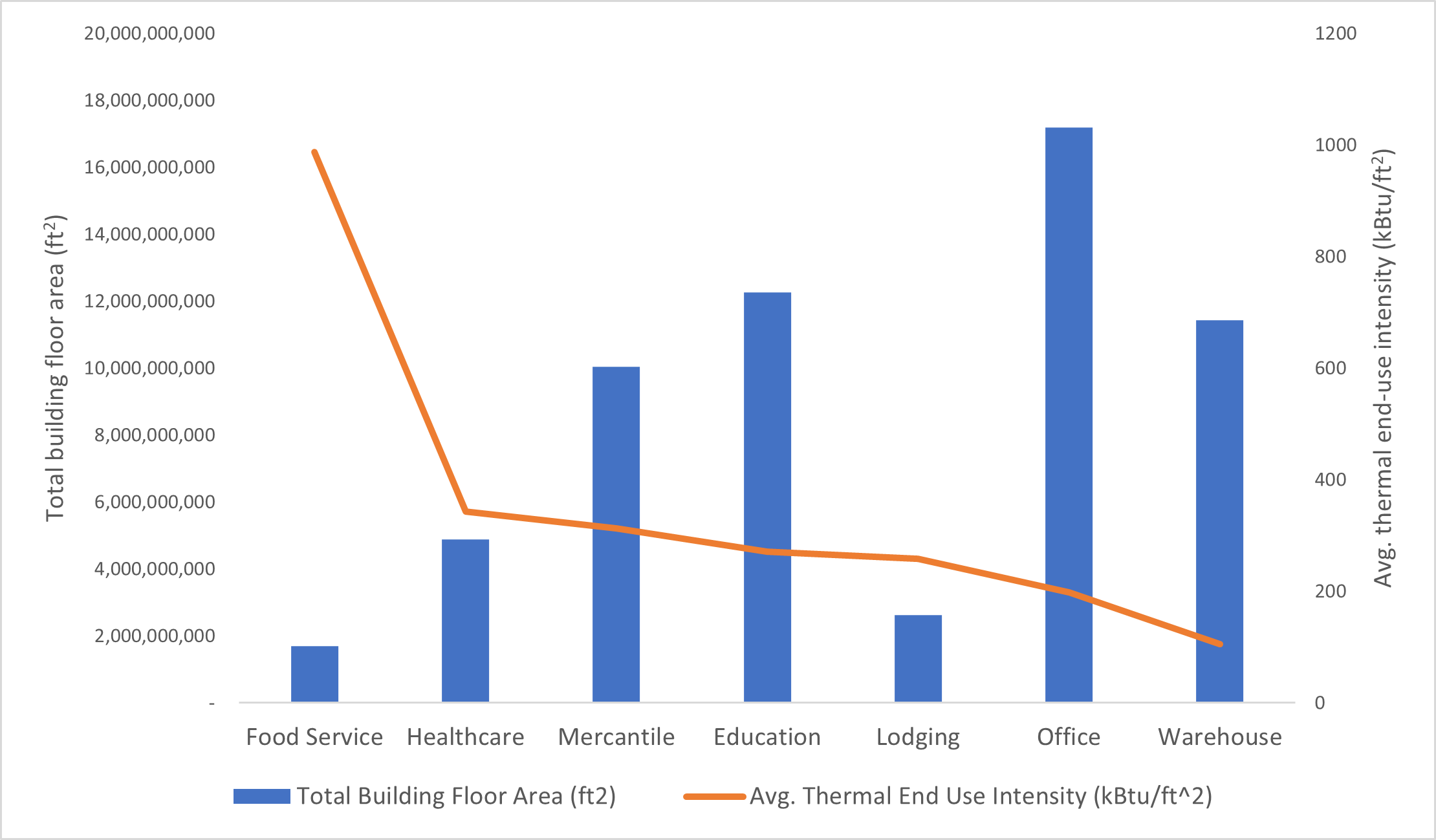

Large commercial office buildings offer an example of a real estate subsegment where markets can serve as an acceleration lever for decarbonization technologies. While office buildings are the largest subsegment of commercial buildings, they have a very low energy use intensity. In other words, compared to other subsegments of real estate, office buildings are more efficient (Exhibit 3 below). In addition, offices already use the smallest percentage of fossil fuels in their operations. To use terminology from Exhibit 1 above, office buildings have already made significant progress toward becoming NZC efficient and NZC ready.

Exhibit 3: Commercial Real Estate Energy Intensity by Real Estate Subsegment

Most of the largest office-specific real estate investment trusts, which are some of the largest owners of office buildings in the United States, talk extensively about sustainability — from explicit carbon neutrality commitments to “push[ing] the envelope on sustainable building design and operations.” It is not a big stretch for new office buildings to entirely electrify in the near future, which will send a clear demand signal to producers. Producer demand in the large office market will, in turn, drive down prices, allowing for adoption of the same technologies in smaller buildings and in other real estate subsegments.

Offices are just one example. Other real estate subsegments offer their own financial and carbon breakdowns that point to the right actors to engage with to accelerate decarbonization. In addition, segmentation analysis of this kind allows financial actors themselves to set net-zero targets in real estate in a more effective, nuanced way by developing customized target pathways reflective of each bank’s portfolio mix.

Inefficient Buildings Are a Liability. Finance Can Help

Every building constructed with fossil fuel technology that will become obsolete creates a future retrofit cost that will be borne by the owners and tenants of those properties. Every time a replacement gas furnace is installed, the building creates an embedded liability to replace that equipment, as well as locking in a volatile and dangerous fuel choice that will be an economic drag into the future.

We must lean into interventions that move critical building decarbonization technologies further up their respective learning curves. To do so, we must first understand the carbon profile and ownership structure of each real estate subsegment, and then understand where finance can provide targeted interventions to speed up the journey of building decarbonization technologies becoming a cheap, default choice for all.

We will share updates as our work progresses. To stay connected with our real estate finance work, follow us on LinkedIn.

Related Insights

Improving Energy Transition Assessments with Regional Pathways

What Michigan’s Clean Community Financing Ecosystem Can Teach Other US Regions

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.