Learn how we are working to transform how we use and produce energy.

French Government Puts US Gas Imports on Ice

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

A move by one of the largest European energy companies shows that both markets and governments are beginning to pay attention to methane emissions and factor them into business decisions. France’s Engie has halted its commitment to a long-term US liquefied natural gas (LNG) import contract with NextDecade Corp estimated at US$7 billion.

This is being done under pressure from the French Government, which holds a 23.6% stake in Engie. The delay was driven in large part by concerns over the greenhouse gas (GHG) emissions of US gas production, particularly from the Permian Basin, which will feed NextDecade’s proposed Rio Grande LNG export plant in Texas. While we cannot ignore the geopolitical considerations also at play, these concerns reflect the growing consensus that all natural gas cannot be seen as equal in terms of its impact on the climate.

There has long been debate about reducing emissions within the oil and gas sector. Earlier this year, Singapore’s biggest buyer of LNG, Pavilion Energy Pte Ltd, asked all LNG sellers to quantify the GHG emissions associated with each LNG cargo produced, transported, and imported into Singapore.

EU Methane Strategy Looms Large

This latest halted contract comes on the back of the European Commission’s (EC) newly proposed EU Methane Strategy, which is part of the European Green Deal. The Strategy prioritizes improved measurement and reporting of emissions of methane, a powerful climate pollutant, for member states and the international community. In the recent announcement, the EC called out energy imports as a major source of methane emissions, and committed to explore possible targets, incentives, or standards for energy imports into the EU.

Engie’s decision demonstrates a trend toward increased scrutiny of gas deals within and beyond the EU. From the outside looking in, the United States does not seem to stand up to such scrutiny. The Trump Administration’s rollback of many climate policies and EPA rulings, including those pertaining to oil and gas methane emissions reporting, monitoring and repair, are just a few of the nearly 100 environmental rules which are being dismantled.

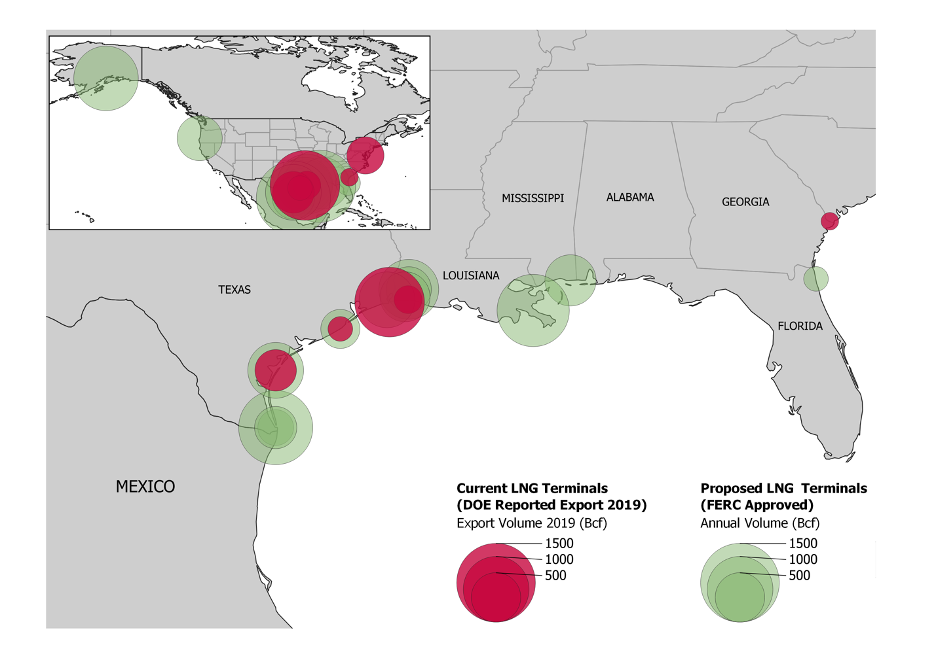

Continuing down this route may make it difficult for US gas producers and exporters to lock in deals with overseas markets, which could have big economic consequences for the US gas industry. In 2019, 38 percent of the United States’ domestically produced LNG was exported to Europe, equating to approximately $2.9 billion dollars in revenue (based on the median 2019 price at export). The export volume to Europe has increased substantially over the last 5 years, paving the way for the approval of 15 new LNG export terminals in North America beyond the six main terminals that exist today. These new terminal projects may face delays or even cancellation of final investment decisions based on the market’s consideration of climate impact.

Market-Based Abatement

However, the US oil and gas industry is stepping up action in spite of federal rollbacks of methane regulation. A number of energy companies have made voluntary commitments to reduce GHG emissions, and methane in particular, in the past few years as a way of demonstrating their commitment to tackling climate change.

These voluntary actions are a step in the right direction, but the industry can and needs to do more to maintain its social license to operate. A market-based approach to abatement, working alongside regulation and voluntary action, can engender the additional accountability and transparency that the industry needs. Without this, companies will continue to fall short of delivering the step change needed for a significant reduction in emissions.

With the right incentives and accountability frameworks, the global oil and gas industry can rapidly and substantially reduce their GHG emissions. We therefore need:

- a credible standard to differentiate global natural gas supply by its climate impact and specifically certify its methane emissions performance; and

- a trusted source of transparent and accessible data, coupled with insightful analytics, that can translate data into opportunities for methane abatement action by operators, investors, consumers, and regulators.

RMI’s work with its European partner, Systemiq, is focused squarely in these two areas. The creation of a global methane emissions standard for differentiated natural gas, coupled with solid climate intelligence from the Climate Action Engine’s novel data-driven approaches to emissions transparency and prediction, can enable the reductions we need in the next decade to meet our climate goals. This work depends not only on solid data, including that collected by academics and NGO partners, but also the independent validation, verification, and communication of these metrics to the global community for action.

Reducing methane emissions from oil and gas operations is among the most significant actions we can take in the near term to help avert catastrophic climate change and improve the environmental performance of a fuel source that will continue to play an important role as we transition to renewable energy. Markets and governments are starting to pay attention to, and make decisions around, what makes gas acceptable today.

However, we know that regulation takes time and we need to act quickly to ensure we can limit global temperature rise. We are encouraged by the steps taken by Engie and Pavilion and we support the efforts of the entire sector in reducing emissions. A globally applicable certification system and real climate intelligence will help these organizations go further in the near term by providing a universal standard that levels the international playing field and ensures everyone is assessed by the same rules.

Authors

Georges Tijbosch

Chathurika Gamage

Related Insights

The World Wastes More Gas Each Year Than the Strait of Hormuz Supplies

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.