Learn how we are working to transform how we use and produce energy.

How the Net-Zero Banking Alliance Helps Banks Set Interim Emissions Targets

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

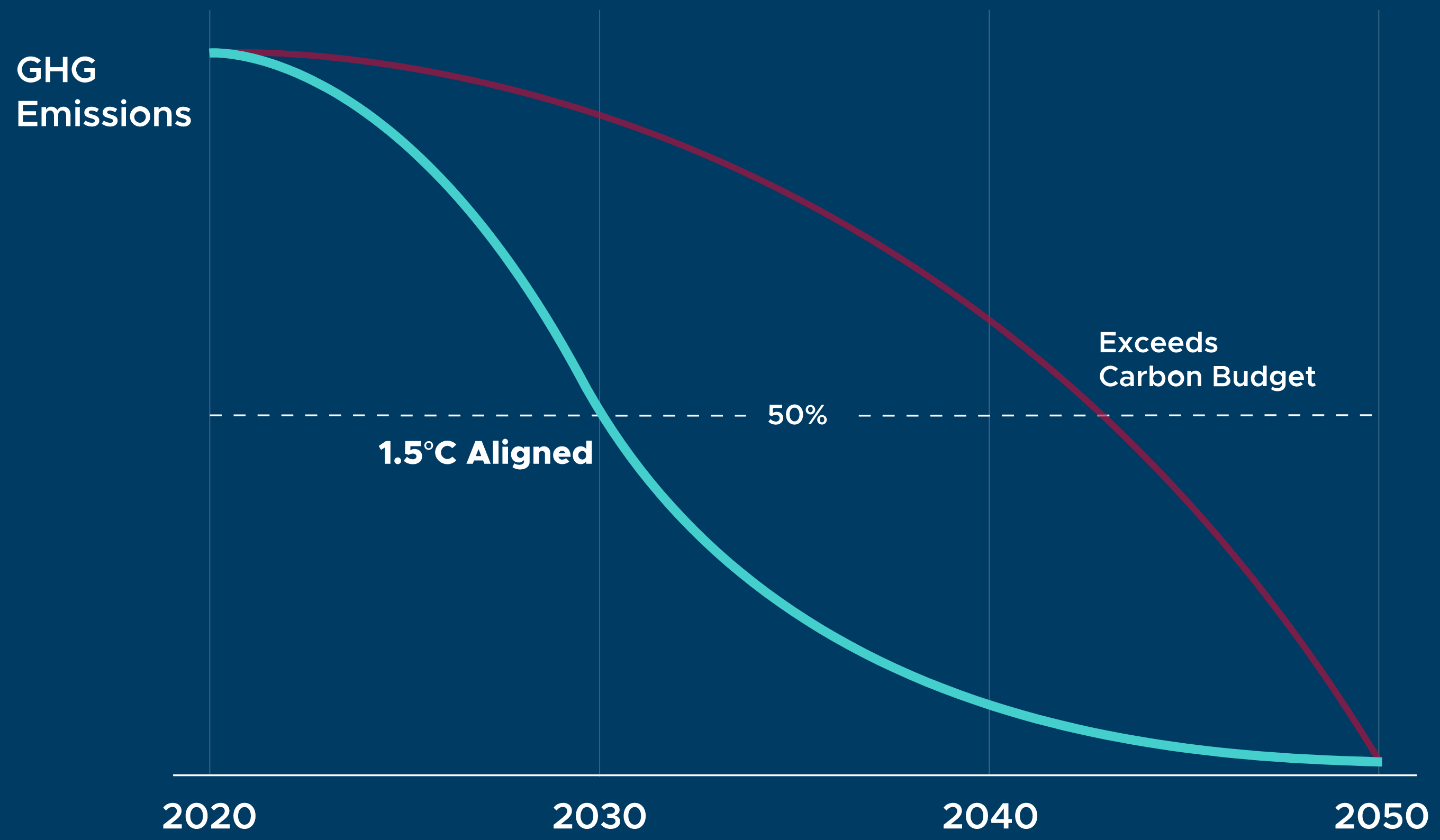

If the last 18 months of banks’ climate ambitions were about announcing 2050 net-zero emissions pledges, the next 18 must be about setting interim targets. Committing to align portfolios with net zero by 2050 is a welcome market signal—but the material question remains where banks intend to be in 1, 5, or 10 years toward that goal. In other words, you’ve announced where you’re going, but how will you get there?

The interim details matter, because turning ambition into action—for banks and their clients alike—means translating long-term 2050 targets into near-term milestones relevant for financial decision-making today. Further, staying within the bounds of our global carbon budget over time requires meeting certain emissions reduction milestones by certain times on our way to zero. Interim targets are therefore essential for assessing the shape of banks’ emissions trajectories.

Enter the Net-Zero Banking Alliance (NZBA), launched April 21, and its focus on setting interim targets. Alongside their 2050 commitments, which must cover all emissions scopes, NZBA’s 43 banking signatories—including Bank of America, Citi, and Morgan Stanley—are required to set 2030 emissions goals. The increasing granularity required of financial institutions’ climate commitments is a necessary step forward in the financial sector’s approach to climate alignment.

How can initiatives like NZBA help global banks set—and, more importantly, implement—their net-zero ambitions? Let’s take a look.

Meaning and Substance

NZBA members commit to aligning operational and attributable emissions from their portfolios with pathways to net zero by 2050 or sooner, in line with 1.5°C temperature targets. But NZBA is more than a platform for high-level commitments. Within 18 months of signing on, member banks must set interim (2030 or sooner) targets in 5-year increments for their most GHG-intensive sectors. Further, within 36 months, members must set targets grounded in climate science for high-emitting sectors like agriculture, fossil fuels (coal, oil, and gas), commercial and residential real estate, power generation, cement, iron and steel, aluminum, pulp and paper, and transportation. NZBA banks must also, among other things, commit to taking a robust approach to offsets and adhering to guidelines for annual disclosures.

A central part of the NZBA commitment is an agreement to follow the UN Environment Programme Finance Initiative (UNEP FI) Guidelines for Climate Target Setting for Banks, also announced April 21. These bank-led guidelines give more meaning and substance to banks’ temporal and sectoral targets. They are rooted in the idea that banks have a key role to play in contributing to the global low-carbon transition, and that a commitment to climate targets is a commitment to achieving impact in the real economy. The guidelines can be applied to banks’ Paris-aligned or net-zero-by-2050 targets to support a temperature goal of 1.5°C in the real economy. NZBA’s objective is to deliver guidelines that are internationally consistent but that can be adapted by country chapters to support local implementation.

NZBA members represent $28.5 trillion in assets and include many members of the 38-bank Collective Commitment to Climate Action (CCCA), another UNEP FI initiative that comprises mainly European firms. CCCA members control $15 trillion in assets and are also required to set sector-specific emissions targets and report on their implementation every two years. CCCA members developed the aforementioned Guidelines for Climate Target Setting for Banks, but not all CCCA members are in NZBA. We will be keeping track of the overlapping initiatives and memberships and are eager to see how the CCCA and NZBA platforms (and members) will coordinate to harmonize action across the banking sector.

NZBA is convened by UNEP FI and co-launched with banks from the Financial Services Taskforce, an industry subgroup of the Prince of Wales’s Sustainable Markets Initiative (SMI). But, importantly, NZBA is an industry-led effort that resulted from months of collaborative efforts across a collection of industry stakeholders. One unsung hero in setting up NZBA was US-based Amalgamated Bank, a union-owned bank with $6 billion in total assets. Amalgamated helped to coordinate CCCA’s move to net zero, co-draft the target setting guidelines, align CCCA with SMI banks, and recruit larger US banks into NZBA.

The aim is that more global banks can join NZBA by COP26 in Glasgow this November and, in doing so, further expand and enrich today’s landscape of climate commitments from global banks.

Conducting the Orchestra

Mark Carney, the UN Special Envoy on Climate Action and Finance, unveiled the NZBA as a sub-initiative of the Glasgow Financial Alliance for Net Zero (GFANZ) platform. In collaboration with the UNFCCC’s Race to Zero (RtZ) campaign, GFANZ comprises and coordinates financial subsector alliances of asset owners, asset managers, banks, and insurers.

Alongside the existing Net Zero Asset Owners Alliance (for asset owners) and Net Zero Asset Managers initiative (for asset managers) and the newly launched NZBA for banks, GFANZ will also create the Net-Zero Insurance Alliance (NZIA) for insurers and reinsurers. NZIA, chaired by French insurance giant AXA, is set for launch at COP26. Leaders across the financial sector will be hoping these latest acronyms make the “climate finance alphabet soup” taste a little bit better.

In total, GFANZ will aim to coordinate efforts across 160 financial institutions, representing over $70 trillion in assets—for scale, that’s over twice the US national debt. GFANZ helps individual firms connect to larger movements and to build capacity. For instance, various new tools and methodologies require heavy quantitative expertise, and instead of doing the heavy lifts themselves, banks can leverage the expertise and capacities of these platforms.

GFANZ arrives on the scene with a hefty agenda. However, as a “coordinator of efforts,” GFANZ is not itself a commitment platform (where firms pledge to achieve goals) nor an action platform (where firms commit to reporting on progress). Rather, GFANZ was designed to:

- Broaden RtZ to all subsectors of the financial system (e.g., by establishing net-zero banking and insurance alliances to complement existing platforms for asset managers and asset owners)

- Increase the number of financial institutions with credible 2050 net-zero commitments by growing participation in the subsector net-zero alliances

- Ensure commitments have robust interim targets

- Coordinate support from financial sector enablers like rating agencies, auditors, and stock exchanges

- Support technical collaboration on cross-cutting issues

- Advocate for supportive policy

Overall, GFANZ seems to be carving itself the role of conductor for the orchestra of net-zero financial alliances. As RMI’s Center for Climate-Aligned Finance highlighted in our Zeroing In report, different types of private financial institutions face unique barriers along the path to a 1.5°C-aligned financial sector, and they have different levers of influence at their disposal for contributing to decarbonization in the real economy. GFANZ’s role is to unite distinct subsector efforts and move private capital in the same direction—under the same set of guiding principles—while being a strong partner to governments as they reshape economic policy.

Conclusion

In just a short while, a pledge of net zero went from the bleeding edge of ambition to a necessary first step. The focus now shifts to targets that contain sufficient detail to measure progress within a timetable that allows for a correction of strategy, if needed. We need banks to act as quickly. Efforts like NZBA promote a common understanding of how to set climate targets, thereby increasing confidence in these pledges, providing stronger signals to clients, and building a foundation for further steps.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.