Learn how we are working to transform how we use and produce energy.

Greening India’s Homes and Vehicles with Low-Cost Finance

Greater Credit from Financial Institutions Can Improve Affordability, Awareness, and Adoption

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Pursuing low-carbon development is central to India’s Paris Agreement climate goals. In this pursuit, net-zero energy buildings (NZEBs) and electric vehicles (EVs) are the two high-leverage areas. The ability to deliver vast emissions reductions across rural and urban settings has brought NZEBs and EVs to the center of the climate change mitigation agenda. In the Indian context, vehicles and homes also have the distinction of being the two most important purchases consumers make.

Once purchased, assets such as gasoline-powered cars and energy-guzzling homes can be hard for consumers to change, thereby locking in emissions for several decades. Getting it right the first time thus proves especially important.

Lower operational costs for adopters are one of the key advantages of both EVs and NZEBs. However, the upfront cost of both NZEBs and EVs remains a barrier, stalling mass adoption. Price-conscious Indian consumers naturally ask: Who will pay for the gap between conventional and greener alternatives?

Central and state subsidies are already playing a role in bridging the cost premium between vehicles running on gas/diesel and EVs. Buildings certified under various rating programs such as the Indian Green Building Council (IGBC) and Green Rating for Integrated Habitat Assessment (GRIHA) are increasingly being allocated incentives by different government entities. In both cases, this government assistance has helped create momentum. However, there exists an oft-overlooked opportunity to reduce the cost premium and improve the attractiveness of both EVs and NZEBs—retail finance.

Retail Finance Can Improve Affordability, Awareness, and Adoption

Retail finance is a key driver of economic growth. Access to credit (in the form of mortgages and loans) has made homes and vehicles more affordable, enabling millions of first-time buyers.

In March 2021, the outstanding housing loans in India amounted to US$298 billion and vehicle loans to US$61.7 billion. Retail banking overall forms a fifth of all bank credits (not including the non-banking financial companies or NBFCs). This large market size is indicative of the influence that financial institutions (FIs) can have on transitioning India’s vehicle and housing stock to greener alternatives.

Dedicated “green” loans or mortgages with affordable interest rates and long tenures can help borrowers spread cost premiums across time. Lower operational costs of EVs or NZEBs improve the ability of the borrower to afford equated monthly installments. This reduces the probability of default, creating a win-win scenario for both the FI and the borrower.

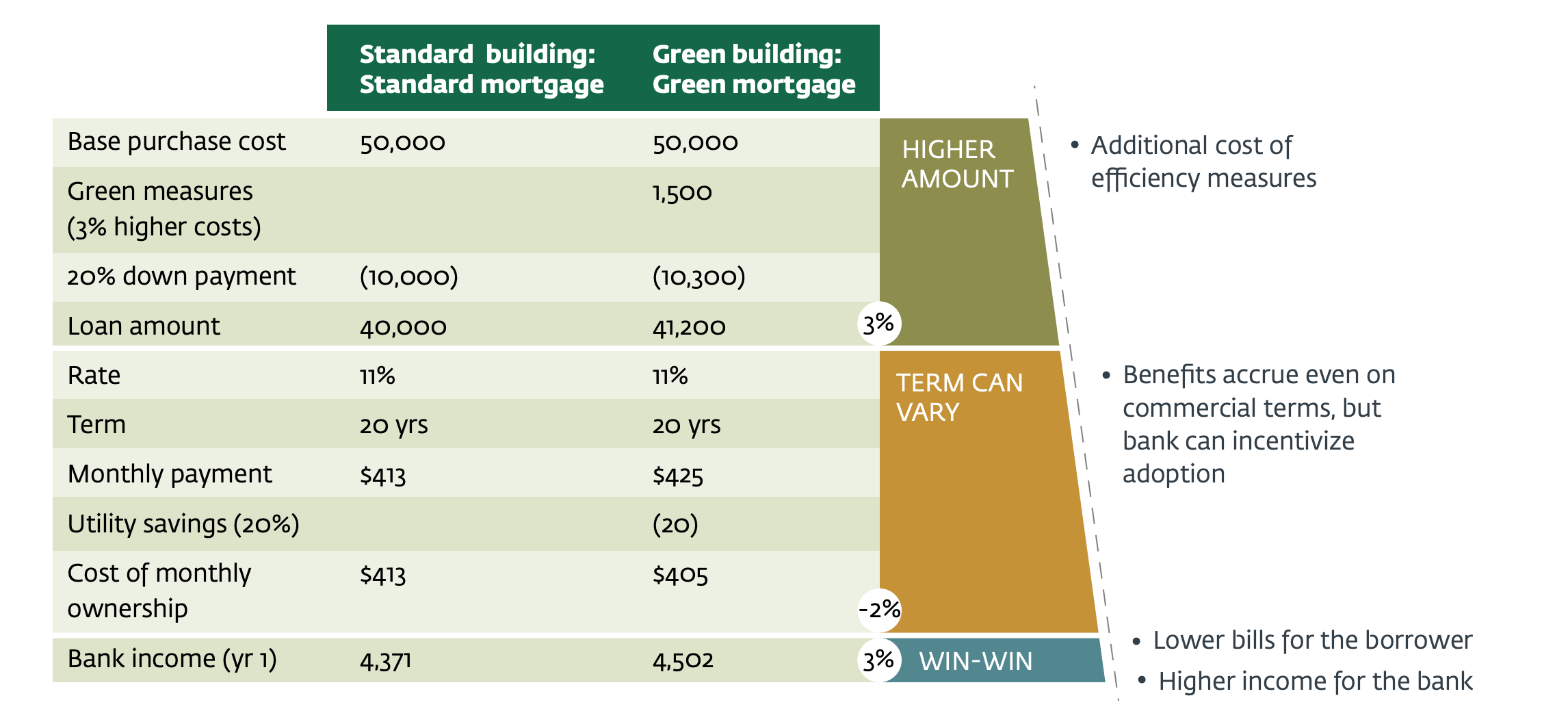

The mortgage example structure in Exhibit 1 shows how a green building can make ownership affordable for the borrower while realizing higher incomes for a bank. Longer tenures can be even more advantageous for both.

Exhibit 1: Green mortgage illustrative example for first year (in $). Source: Modified from IFC, 2019

Affordability is only part of the possible impact. FIs also have the potential to enhance consumer awareness. Commercial banks and NBFCs are in regular contact with individuals interested in purchasing new assets. This channel can be instrumental in communicating the financial benefits of EVs or NZEBs and busting myths on ownership. The resulting behavioral change on purchase decisions has the potential of raising the aspirational value and desirability of green assets. Hence, by improving affordability and awareness, FIs can help scale adoption.

Solutions Exist but Risks Need to Be Overcome

Dedicated green loans and mortgages are not new inventions. In India, too, a few forward-thinking FIs have started developing these products. For example, the State Bank of India has launched a Green Car Loan, whereas the National Housing Bank’s SUNREF India program is facilitating affordable green housing credit worth ₹800 crore (US$107 million) in India.

Replicating such products across the retail finance ecosystem requires us to consider current barriers. Unique challenges exist: For EVs, the lack of secondary market is a concern. Meanwhile for NZEBs, developers lack incentives to construct property where operational benefits will pass on to the occupant. However, many risks are common. In both cases, unproven asset value, low awareness of techno-economics, and an uncertain policy environment are seen to be holding back finance.

Moving forward, overcoming these barriers will be important for unlocking the opportunity inherent in greening retail finance. Building the capacity of FIs for developments in EVs and NZEBs will be needed to maximize the potential of dedicated loan or mortgage products. Another common area that needs to be prioritized is data availability on loan performance of EVs and NZEBs. To this end, the Reserve Bank of India (RBI) can designate green assets such as EVs and NZEBs as financial reporting sub-sectors.

Also, the RBI can consider the creation of a sustainable finance taxonomy by setting baselines and definitions for green assets. This will help develop insights into existing green financial products and direct finance to the most effective technologies.

The vehicle and housing finance industries can simultaneously learn from each other. For example, the Government of India’s Partial Risk Sharing Facility for Energy Efficiency is a promising instrument enabling FIs to lend to energy-efficient projects. Risks of financing energy service companies wishing to retrofit buildings are partially covered under this facility, reducing overall transaction costs. Such risk-sharing programs need to be introduced for EVs as well to improve the lending confidence of FIs.

For EVs, partnerships between FIs and manufacturers help mainstream low-cost financing. Developer-FI partnerships for net-zero energy housing similarly need to be scaled. IIFL Home Finance is an FI already piloting green certification and lending programs with local developers in Indian cities. Providing technical assistance and data-driven support to the value chain is helping develop a pipeline of NZEBs.

Governments can enable more such partnerships by offering interest rate subventions, stamp duty reductions, and incentives for longer tenures. Creating a shared roadmap for the development of NZEBs will additionally provide direction to the entire ecosystem.

Financial Institutions that Take the Lead, Can Reap the Rewards

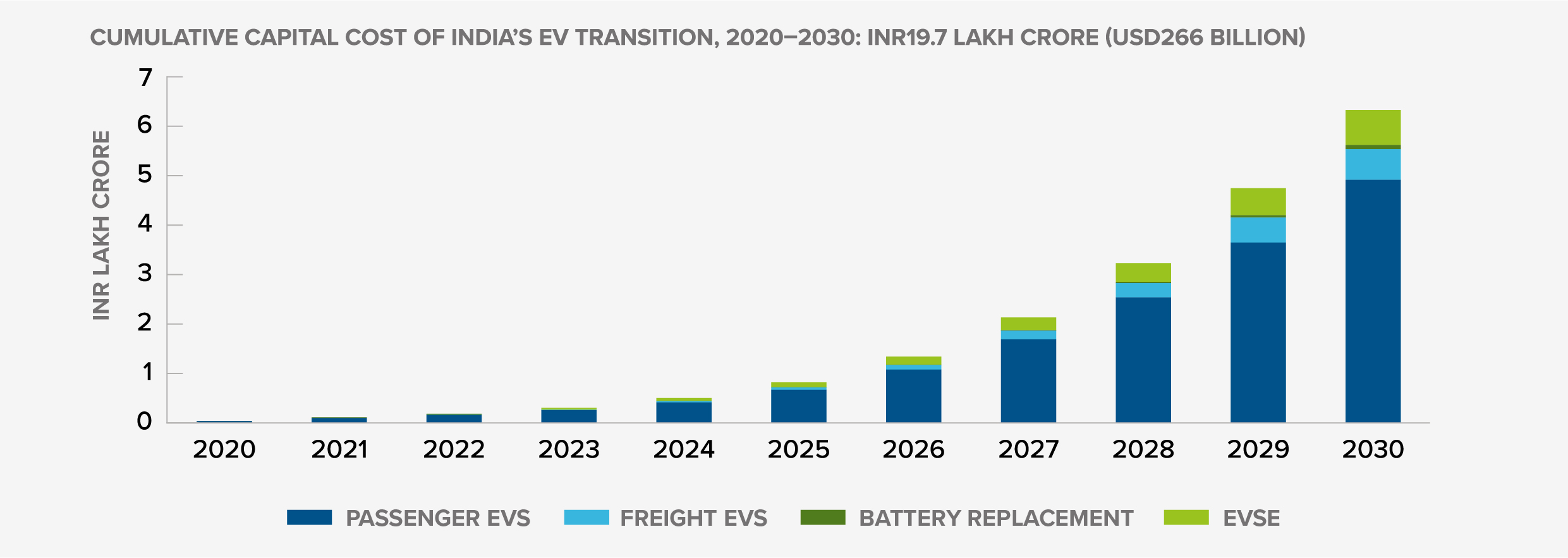

For EVs alone, the cumulative capital investment required by the end of the decade could be as much as US$266 billion (see Exhibit 2). This translates to a loan market of US$50 billion in 2030. Similarly, estimates suggest a US$1.25 trillion investment opportunity in green housing by 2030. FIs that champion green loans and mortgages and proactively enable the market stand to gain the most in these scenarios.

Exhibit 2: Cumulative capital cost of India’s EV transition, 2020–2030, including EVs, batteries, and electric vehicle supply equipment. Source: NITI Aayog and RMI, 2021

Energy transition-related risks will also make EVs or NZEBs more worthwhile to lend to in the near-term. Many of the gas/diesel vehicles that FIs are financing today will start to lose their value as the upfront cost of EVs decreases, emission norms are tightened, and fuel prices increase.

Similarly, as the Energy Conservation Building Code for residential buildings is notified across India and incentive structures are enhanced, the possibility of stranded real estate assets may increase. Resilience and energy cost volatility risks should also be considered.

The RBI has already begun to commit to climate action: in April 2021, it joined the Network for Greening the Financial System, a green finance coalition for central banks. This commitment signals the inevitability of green finance in India, of which green lending will be an essential part. Most recently, the Climate Finance Leadership Initiative’s launch in India is demonstrative of the financial potential to accelerate mass consumer adoption of green assets such as EVs and NZEBs, leading the country closer to Paris Agreement goals. With the stage being set, now retail finance must step up.

Authors

RMI India

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.