Learn how we are working to transform how we use and produce energy.

US Homeowners and Lenders Face Rising Risks from Extreme Weather

To fortify low-income communities, the climate bill extends financing and grants

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The Inflation Reduction Act, signed into law on August 16, 2022, includes critical funding for homeowners to prepare their properties for climate adaptation in the face of extreme weather. Detailed in the 800-plus-page package:

- Over $3 billion in block grants for environmental and climate justice.

- $1 billion in grants and loans for energy efficiency, water efficiency, and climate resilience efforts in affordable housing.

- Roughly $2.6 billion for the National Oceanic and Atmospheric Administration (NOAA) to support community resilience efforts to prepare communities and homeowners for the worsening impacts of extreme weather.

This historic bill is a giant step in the right direction to future-proof thousands of communities. For this wave of money to make its greatest impact, the next step is to begin to build greater understanding and provide more information to homeowners so they can make more informed decisions prior to property acquisition.

In the wake of more frequent extreme weather events, especially as we head into peak Atlantic hurricane season and are in the midst of another growing wildfire season, many homeowners are at risk of facing major climate-related damage to their properties. As a result, the financial health of US households and the entire mortgage industry supporting our nation’s housing market are under threat.

Through collective action and leadership from key industry stakeholders, policymakers, and regulators, we can ensure allAmericans have equitable access to tools and innovative financing solutions to future-proof their home assets against extreme weather events and volatile energy costs.

Understanding Financial Risks for Climate Vulnerable Homes

Homeowners, particularly low-income families and communities of color are increasingly subject to financial risks to property value, the potential for skyrocketing insurance premiums, and volatile utility costs because of climate-related hazards. The First Street Foundation, which models property-level climate risks, found that in the United States over 79 million properties today face some level of wildfire risk and more than 14.6 million properties are susceptible to substantial flood damage.

Focusing on one of the most climate-vulnerable states, a study by McKinsey & Company concluded the property loss rate in southern Florida could reach the level of the Great Recession by 2030 due to flooding from sea level rise — and it could potentially triple that number if combined with a financial downturn. Properties in the state exposed to disruptive flooding could lose between 5 and 15 percent of their value in the next decade when compared with similar unaffected properties, the authors found.

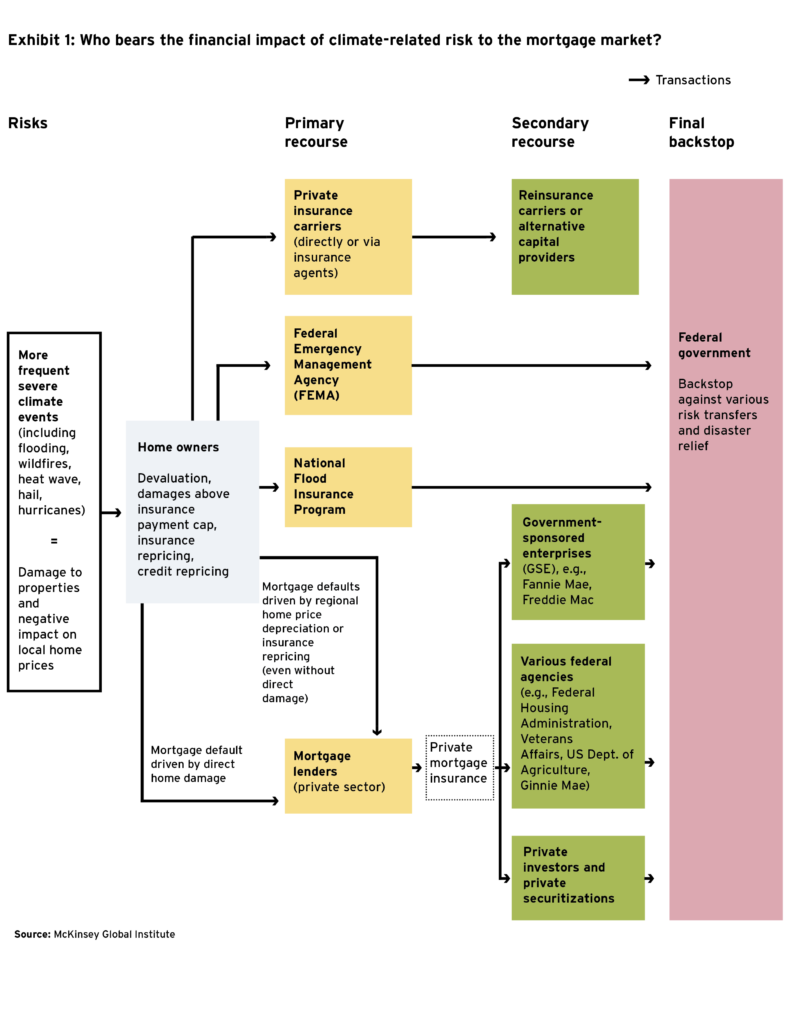

As these impacts ripple through the market, mortgage market actors and homeowners will bear the weight of increased costs and losses. Additionally, insurers, lenders, federal actors, guarantors, and the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac — which back approximately 63 percent of all mortgage origins nationwide — are also at risk of assuming the financing burdens associated with increased delinquency rates, portfolio risks, and decreased asset valuations. Past climate events have already negatively impacted many of these housing actors. For example, after Hurricane Harvey struck Texas and Louisiana in 2017, mortgage delinquency rates nearly doubled in the most flood-exposed neighborhoods.

As depicted below, a broad set of housing stakeholders share some part of the financial risk, including the federal government, which acts as the final backstop on defaulted government-insured and GSE mortgages in addition to paying out disaster relief.

Environmental Justice and Housing Inequity Impacts of Extreme Weather

Extreme weather also exacerbates the ramifications of structural racism, as historically redlined and underserved communities are often the ones hardest hit. An analysis of $31 billion in flood claims paid by the National Flood Insurance Program between 2010 and 2019 found that damages disproportionately occurred in zip codes with more than 25 percent Black residents. During Hurricane Katrina, homes owned by Black residents were three times as likely to experience flood impacts. And in the Houston neighborhood that suffered the worst flooding damage following Hurricane Harvey, 49 percent of residents were non-White.

While the risks and inequities at stake are substantial, the opportunities to drive forward leadership and policies to address these challenges remain plentiful. Although more research needs to be conducted to fully understand and assess the threat climate events pose to the industry, homeowners and industry actors can take action today to make more informed decisions about their future investments.

Leveraging Data and Research to Achieve Equitable Pathways to Homeownership

All home buyers and homeowners should have access to data to better understand and assess the potential climate-related risks their property may face. The Consumer Financial Protection Bureau (CFPB) amplified this call, emphasizing that the capture and disclosure of property-level climate-related data is sorely overdue and would provide a necessary initial step toward addressing blind spots consumers face across the marketplace.

Today, homeowners and buyers can leverage some publicly available tools on their own, such as FEMA’s National Risk Index, USDA Wildfire Risk to Communities, ClimateCheck®, and Risk Factor™, to better understand the potential risk scenarios their property may face. However, additional research and policy analysis is needed to effectively address the potentially inequitable outcomes that may result from broader use of property risk data and disclosure in appraisal and underwriting standards, including how to avoid devaluing properties in already underserved communities.

Financing a More Resilient Future for Homeownership

Providing homebuyers, homeowners, and housing market actors with information to accurately evaluate the true cost of homeownership empowers them to act. Climate-vulnerable homes can be cost-effectively retrofitted to reduce potential climate-induced damage.

An exhaustive cost-benefit analysis of natural hazard mitigation found that every dollar invested in home retrofits to protect against floods and hurricanes can save $6; every dollar invested in retrofits to protect against fires and earthquakes can save $2 and $13, respectively.

With improved clarity regarding the costs and benefits of climate-aligned housing, homebuyers and homeowners have a number of resources from which to draw — including the Weatherization Assistance Program, state and local resiliency incentive programs, insurance discount programs, Hazard Mitigation Assistance Grants, and low-interest disaster mitigation loans —in addition to new funding sources laid out in the Inflation Reduction Act. Additionally, green and rehabilitation mortgage offerings, such as Fannie Mae’s HomeStyle® Energy mortgage or Freddie Mac’s CHOICERenovation® mortgage, can enable mitigation measures to be rolled into a mortgage at the time of purchase or refinance. All of these programs and tools can act as the bridge to ensuring that tens of millions of homes across the United States are more resilient to current and future risks from climate disasters.

Accelerating Progress to Climate-Align the Housing Market

Leveraging existing low- or no-cost financing tools and requiring climate-related home performance and resilience data are essential initial steps. But strong leadership and guidance from industry players, policymakers, and regulators — including the Federal Housing Finance Agency, banking regulators, lenders, and the CFPB — are necessary to help the US housing market mitigate current and future climate-related financial risks. We need policies, resources, and actions to steer the industry on a path toward future-proofing tens of millions of existing American homes, while expanding more equitable access to homeownership through coordinated financing programs at the time of transaction. The opportunity to ensure that communities across the United States remain resilient to current and future climate impacts is a sizable one — and the time to act on it is now.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.