Large view on the powerlines and the windmills on the field

Five Reasons Your Company Should Buy Off-site Renewables in 2017

Guest author Scott Macmurdo is a sustainability specialist with NRG Energy, which is a founding sponsor of the Business Renewables Center.

Guest author Patrick Molloy is a financial analyst at the Business Renewables Center.

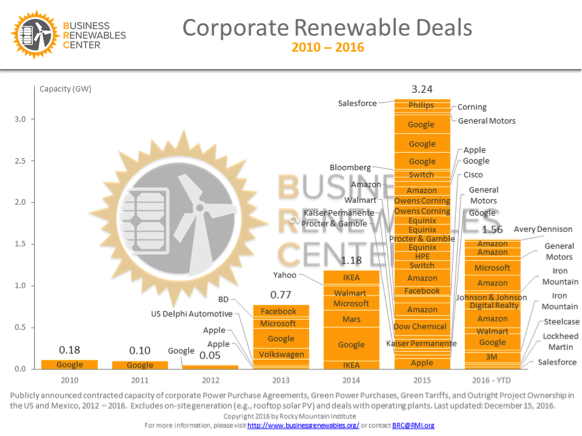

Corporate interest in renewable energy is skyrocketing as companies realize that off-site projects can offer the flexibility and scale necessary to meet their needs. Companies contracted for 1.56 GW of off-site renewables in 2016, with almost half (642 MW) coming in the fourth quarter alone (see Figure 1). Purchases by companies outside the tech sector (443 MW) showed that the buying pool is diversifying beyond the usual suspects. More than 80 companies have now committed to purchasing 100 percent renewable energy through RE100, and Rocky Mountain Institute’s Business Renewables Center (BRC) now counts 100 corporate buyers as members.

FIGURE 1

But despite growing interest, less than one-fourth of corporate renewable energy buyers in the BRC’s network have completed an off-site transaction to date—this from a group of companies that are actively looking to participate in the market. If your company has not yet engaged in an off-site renewable energy transaction, here are five reasons why you should get started in 2017:

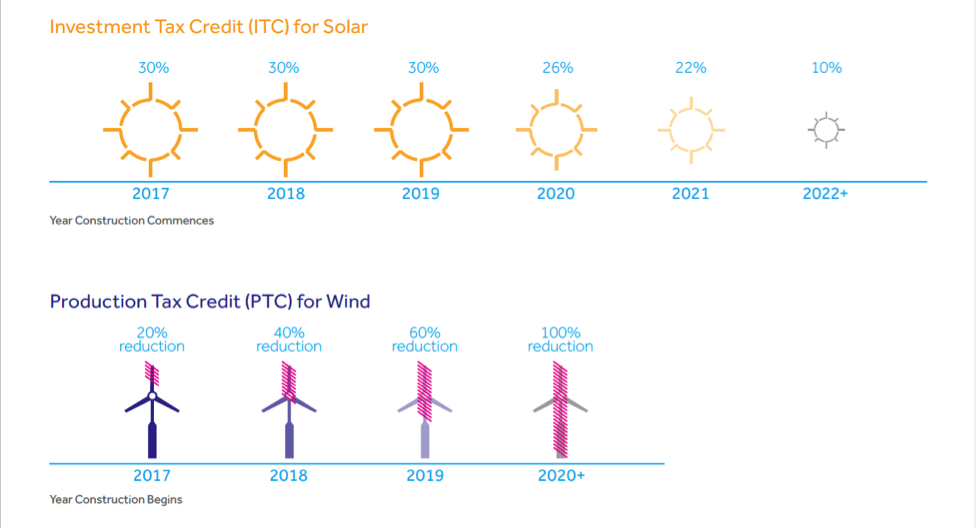

1. Beneficial tax credits are still available

The explosive growth of the off-site market in 2015 happened largely because of companies trying to “beat the clock” before the Renewable Electricity Production Tax Credit (PTC) for wind and Business Energy Investment Tax Credit (ITC) for solar expired at the end of the year. Congress extended these incentives in late December 2015, but it also designed the value of the credits to phase down over time (see Figure 2).

FIGURE 2

Source: NRG Energy

Though the extension of the tax credits is a big win, it doesn’t mean that time is on the buyer’s side. The PTC has already initiated its 20 percent annual decline, meaning that buyers are essentially losing $5 per MWh (half a cent per kWh) in benefits for each year that they wait to buy wind energy. The IRS recently issued Safe Harbor guidance that would, in practice, allow more wind projects to lock in the full PTC value beyond the designated phase-down schedule, but there is no guarantee that buyers will receive the retroactive value of tax credits. Developers may exhaust their supply of grandfathered equipment by the time a contract begins.

Capturing the maximum value of tax benefits is often a make-or-break proposition for renewables projects, because these credits can account for a large share of the revenue that a developer derives from a project. A common misconception is that developers earn most of their revenue through the PPA rate they charge to customers. In fact, a project’s overall value is also tied to depreciation-related tax benefits (MACRS), revenue from the PTC/ITC, and energy sales in the post-contract period. The ramp-down schedules for the PTC and ITC put the impetus on buyers to take action today.

What’s more, although the new presidential administration may bring changes to the energy landscape, corporate interest in renewables should remain strong. At a recent BRC conference for leaders in the corporate renewable energy sector, 92 percent of attendees said that their U.S. renewable energy strategy would see more engagement or remain unchanged after the elections.

Political leaders have signaled that comprehensive corporate tax reform will be a priority in the coming months, but many analysts expect the PTC and ITC to endure due to bipartisan support in the past. It is worth noting that reducing corporate tax rates would make the PTC and ITC less valuable, which might then lead to higher PPA rates. For companies seeking to add renewables to their portfolios, it is advantageous to act while tax credits hold the most value.

2. Interest rates are near historic lows

Interest rate fluctuations significantly affect PPA rates, because the total cost of a renewable energy system is paid almost exclusively up front and amortized over the lifetime of the project. Renewable energy generation has virtually no marginal costs, because the “fuel” is free. Developers finance almost the entire cost of the project up front and pass the costs onto the buyer in the form of the PPA.

The Federal Reserve Board of Governors just raised its target range for the Federal Funds Rate to between 0.5 percent and 0.75 percent in December 2016. This action followed a period from 2008 to 2015 during which rates were at virtually 0 percent. The prospect of higher interest rates means that it makes sense for buyers to pursue projects in the current capital environment where money is likely cheaper than it will be in the future.

Some question whether it makes sense to hold off for a better wind or solar deal in the future given the pace at which technology costs are falling. But hard costs do not tell the full story. On the solar side, hard costs account for about half of the total. The other half comprises so-called soft costs, which are subject to cost inflation tied to broader macroeconomic conditions. So while technology costs may put downward pressure on PPA rates, the countervailing effects of interest rates and tax credit reductions justify getting started in 2017.

3. Historically low electricity rates are not an obstacle

An off-site PPA enables companies to lock in access to power at a known price, creating a hedging opportunity against wholesale electricity price increases. PPAs are generally structured with a fixed price for 15 to 25 years, sometimes with a built-in escalator to keep pace with inflation. Wholesale electricity rates are currently near historic lows, leading some to question the logic of locking in a long-term escalating price in the form of a PPA.

Predictions vary about the future of wholesale electricity prices. The Energy Information Administration expects commercial prices to range between about $103 and $131 per MWh (10.3 to 13.1 cents/KWh) over the coming decades, depending on factors such as fossil-fuel prices and the fate of the Clean Power Plan.

No matter your view of the electricity market’s future, a contract can often be structured to meet your needs. A traditional PPA serves as a hedge against a high-price future scenario by fixing rates at current lows. If your company is worried that flat or declining wholesale prices will make a PPA uncompetitive, protective puts and other financial measures can hedge against such cost exposures. In either case, companies can design their PPAs to match their unique market outlook, hedging appetite, and current position.

4. Transmission line access is still available

Access to transmission line “headroom” is a critical component in determining the overall cost of an off-site renewables project. The best solar and wind resources are often located far from the places where energy is consumed, making it necessary to transmit electricity over great distances. The availability of sites near high-capacity transmission lines is limited, and siting too many projects along a single transmission line can force project owners to curtail generation in a way that ultimately results in higher prices for the consumer. Since transmission line capacity is allocated on a first-come, first-serve basis, companies that move first may be able to capitalize on lower PPA rates.

Several high-profile infrastructure projects highlight the need for more transmission infrastructure to unlock the full potential of renewable energy development in the United States. Some examples include the proposed 3 GW TransWest Express to carry Wyoming wind energy to California, the 4 GW Plains and Eastern Clean Lines to connect Oklahoma wind to bigger load zones, and the 1 GW Champlain Hudson Power Express to carry hydroelectric generation from Quebec to New York. A recent study from the National Renewable Energy Laboratory estimated that high levels of wind penetration would result in curtailment rates of over 7 percent in the West, even if over 10 GW of new transmission infrastructure were built. These trends show that the renewable energy sector needs additional infrastructure to reach its full potential, which is why companies that move forward now will be at an advantage.

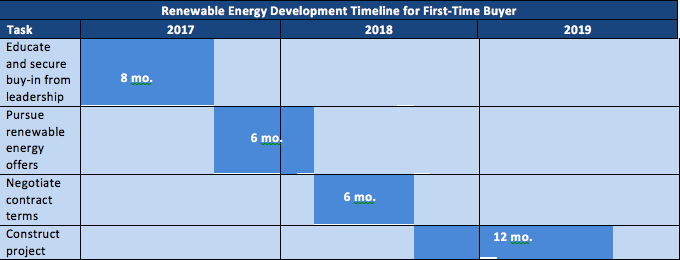

5. 2020 sustainability commitments are coming due

Many companies have set renewable energy or greenhouse gas goals tied to 2020, but have not yet participated in the off-site market. While 2020 may seem like a long way off, companies looking to add renewable energy to their portfolios need to get started now in order to meet their deadlines. The development cycle for large-scale solar and wind projects is a multiyear process (see Figure 3). For first-time buyers, it can take months or even years just to secure buy-in from internal stakeholders in finance, accounting, treasury, legal, and facilities. This means companies that start to look for projects this year may not begin installation until next year, whereas forward-looking companies likely spent 2016 planting seeds that will bear fruit in 2017.

FIGURE 3

Source: NRG Energy

GET STARTED NOW

Some companies question whether a better deal may be just around the corner given tax credit extensions, falling technology costs, and low electricity prices. The validity of this position depends on whether PPA rates will fall fast enough to counteract the effects of the ITC/PTC step-down, interest rate increases, and transmission line issues. Nobody has a crystal ball, but lengthy project development timelines, fast-approaching sustainability goals, and broader economic forces provide compelling reasons to get started in 2017.

Image courtesy of iStock.